Generated Title: Mortgage Rates Are Finally Calming Down. Here’s Why I’m Not Buying It.

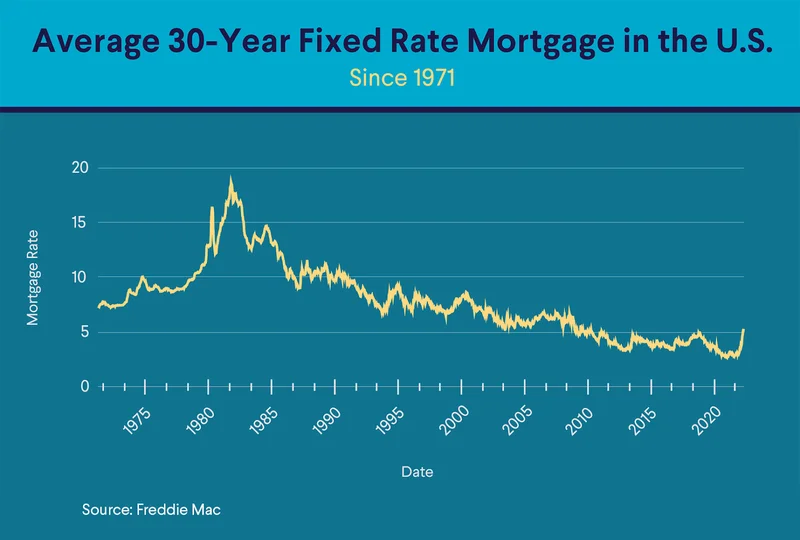

The headlines are practically a sigh of relief. After a turbulent ride that saw rates touch 7%, the mortgage market appears to have found a moment of Zen. According to Freddie Mac, the average 30-year fixed rate has dipped to 6.19%, its lowest point in over a year. Reports like Mortgage and refinance interest rates today, October 24, 2025: Now at a more than a one-year low and data from Zillow and Optimal Blue paint a similar picture, with numbers hovering in a tight range. For the first time in what feels like an eternity, the word “stability” is being used without a hint of irony.

This newfound calm has been attributed to a confluence of factors: inflation is cooling slightly, job growth is moderating, and the Federal Reserve has signaled potential rate cuts on the horizon. Sam Khater, Freddie Mac’s chief economist, noted that this trend has kept refinancings high, accounting for more than half of all mortgage activity for six straight weeks (a clear indicator of homeowner response to even minor rate relief).

On the surface, the data suggests a market settling into a predictable, if elevated, new normal. But when you look past the top-line averages, the foundation of this "calm" starts to look less like solid ground and more like a thin sheet of ice.

The Anatomy of an Illusion

The first discrepancy emerges when you simply try to answer the question: what are mortgage rates today? One source reports 6.19%. Another says 6.13%. A third, more granular data provider, clocks the 30-year conventional rate at 6.159%. While small, these differences highlight a crucial point: there is no single "mortgage rate." The number you see in headlines is a national average, a statistical blend that smooths over significant regional and lender-specific volatility.

I've looked at these reports for years, and while some divergence between sources is expected, the current spread feels symptomatic of a fragmented market, not a cohesive one. It suggests lenders are pricing risk differently, reacting to local economic signals and their own balance sheet pressures. This isn't stability; it's a collection of disparate data points being forced into a tidy narrative.

The market's optimism is largely pinned on future Fed action. The consensus forecast is for a half-point drop in the federal funds rate—or, more accurately, two separate 25 basis point cuts by the end of 2025. But the correlation between the Fed funds rate and 30-year mortgage rates is not one-to-one. Mortgages are priced against the 10-year Treasury yield, which is influenced by a far broader and more chaotic set of inputs, including global investor sentiment and long-term inflation expectations.

We saw this disconnect play out last year, when mortgage rates climbed above 7% even as the Fed was cutting. What happens if the upcoming cuts don't translate into the relief everyone is banking on? What if stubborn inflation, potentially reignited by new tariff policies or labor market shifts, forces the Fed to hold its ground? These aren't fringe possibilities; they are material risks that the current narrative of a calm, gently declining rate environment conveniently ignores.

The New Homebuyer's Gambit

This illusion of stability creates a dangerous dynamic for homebuyers and those looking to refinance. The prevailing wisdom is to lock in a rate now, capturing this moment of tranquility before it vanishes. It feels like a prudent move. After all, a rate of 6.2% on a $328,000 loan (a $410,000 home with 20% down) translates to a monthly payment of about $2,015. At 6.8%, that payment jumps by $130. That’s real money.

But this advice frames the decision as a simple choice between today’s rate and a potentially higher one tomorrow. It overlooks the much larger context. We are still dealing with the "golden handcuffs" phenomenon, where millions of homeowners are locked into sub-3% rates from the pandemic era, effectively freezing a huge portion of housing inventory. This supply constraint is a major reason prices have remained stubbornly high despite the surge in borrowing costs.

So, is locking in a 6.1% rate today a victory? Or is it simply accepting a new, historically expensive baseline? Forecasts from both the Mortgage Bankers Association and Fannie Mae suggest rates will likely remain above 6% for most of 2026, with only a modest dip to 5.9% projected for the final quarter. That isn't a return to normalcy. It's a high-altitude plateau.

This brings us to the core questions the data doesn't answer. Are we witnessing a temporary pause in a longer-term trend of rate normalization, or is this the beginning of a sustained easing cycle? And how much of the recent dip is based on solid economic footing versus speculative hope about the Fed's next move? The stability we see today feels less like a destination and more like a brief layover in an unknown airport.

The Data Points to a Fragile Peace

Let's be clear. The current steadiness in mortgage rates is not a sign of a healthy, settled market. It is a tense equilibrium, a statistical stalemate between cooling inflation and persistent economic uncertainty. The narrative of "calm" is an oversimplification of a deeply complex and fragile system. It’s like looking at a still photograph of a spinning top—the image is static, but the underlying object is in a state of intense, controlled chaos. Any nudge could send it wobbling. For borrowers, acting now isn't about seizing a moment of calm; it's about placing a bet in a market that is anything but.