For decades, the sound of a heavy metal credit card hitting a restaurant table has been a subtle signal of status. It wasn't just a piece of metal; it was a symbol. It meant you were part of a club, one that rewarded high spending and a deep entanglement with the world of credit. That clink was the sound of a system built on a simple, powerful premise: the more you borrow and spend, the more perks you deserve. It was a brilliant model for the banks, but it always tied our aspirations to debt.

I’ve spent my career watching technology dismantle old models, and when I first saw Klarna’s latest announcement, I honestly just sat back in my chair, speechless. The company's move, Klarna Launches Memberships: Premium Perks Without Expensive Credit, is on the surface about a new membership program with shiny metal cards and airport lounge access. But look closer. This isn't just another fintech product. It's a philosophical statement, a quiet revolution that aims to sever the link between financial privilege and credit dependency. What we're witnessing is the great decoupling of status from debt.

A New Value Equation

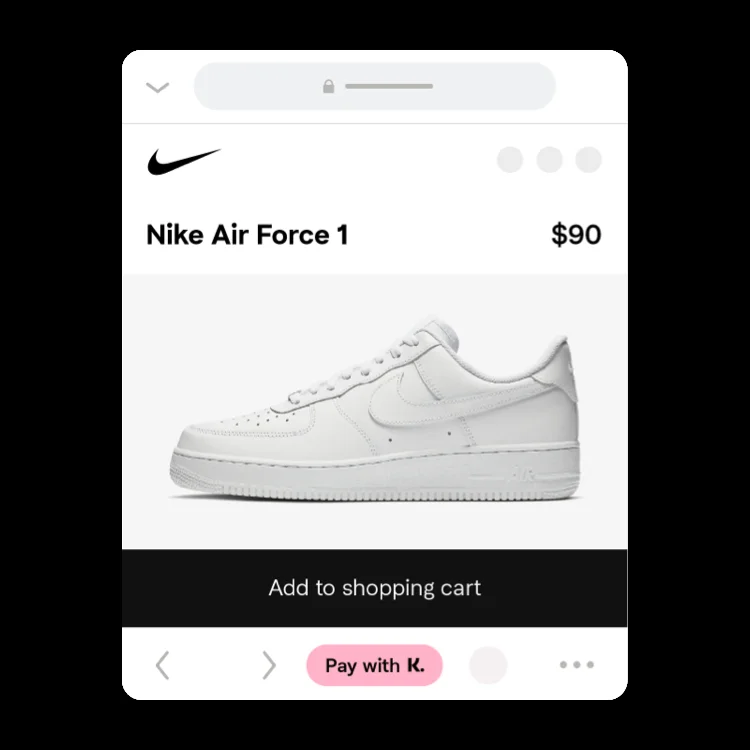

Let's break down what Klarna is actually doing with its new Premium and Max tiers. They’re offering a suite of perks—travel insurance, subscriptions to The New York Times and Vogue, ClassPass memberships, cashback—all for a flat monthly fee. The crucial part? These rewards are tied to your Klarna Card and your Klarna balance. In simpler terms, it's like a digital wallet you top up from your bank account. You’re spending your own money, not borrowing from the bank.

This completely flips the script. The old world said, "Spend thousands on our credit card, accumulate points, and maybe we'll grant you access to our lounge." Klarna is saying, "Here's access to the lounge. The price is €45 a month. No debt required." It transforms perks from a reward for indebtedness into a straightforward consumer product. It's like Netflix for financial benefits.

This is the kind of breakthrough that reminds me why I got into this field in the first place. For years, we’ve talked about democratizing finance, but it often meant just creating slicker apps for the same old systems. This feels different. It’s a direct challenge to the idea that you have to play the credit game to enjoy the benefits of modern financial life. It asks a profound question: Why should access to a better travel experience or premium journalism be contingent on your willingness to carry a balance? Why can't it just be something you choose to buy, like any other service?

Of course, analysts rightly point out that the value must justify the cost. But that's precisely the beauty of this model. It's not a hidden game of interest rates and late fees; it's a transparent value proposition laid bare. You, the user, get to look at the menu of benefits and decide if it's worth the price. The power is finally back in your hands.

The Financial Super App Takes Shape

This move isn't happening in a vacuum. It's the most significant step yet in Klarna's evolution from a simple "Buy Now, Pay Later" button at checkout to a full-blown financial ecosystem. Think about the first mobile phones—their only job was to make calls. Then came the iPhone, which turned the phone into a platform for your entire digital life. Klarna is attempting a similar leap, moving from a single feature to a central platform.

They're building an entire ecosystem where you manage your money, you pay your friends, you get your news from partner subscriptions, you book your travel with airline cashback, you meditate with Headspace—it's a bold move to become the central operating system for a huge part of your life and it's happening right before our eyes. This isn’t just about competing with Afterpay or Affirm anymore; it’s about creating an alternative to your traditional bank account, your Chase Sapphire Reserve, and even your Venmo account, all rolled into one.

With this kind of integration, however, comes a profound responsibility. When one company becomes the hub for so much of our daily activity, questions of data privacy, consumer choice, and algorithmic fairness become absolutely paramount. Building a powerful, all-encompassing platform is one thing; ensuring it remains a force for user empowerment is another. It’s a challenge Klarna must meet head-on as it asks for more of our trust.

Still, the ambition is breathtaking. They are betting that we, the consumers, are ready for a new relationship with our money—one based on direct value and transparent choice, rather than the opaque and often predatory mechanics of the credit industry. The question is no longer just "How does Klarna work?" but "How do we want our financial lives to work in the 21st century?"

The End of the Old Guard?

This is more than just a new card. It's a new blueprint. For decades, the financial world operated on a model of gatekeeping, where the best perks were reserved for those who played the credit game most effectively. Klarna is proposing a different path: a subscription to a better financial life, open to anyone willing to pay the monthly fee. It's a direct, honest transaction. And in a world tired of fine print and hidden costs, that honesty might just be the most disruptive feature of all.